Blue Origin: can capital plus time fix execution?

An IPO CLUB perspective on the hardest question in space investing right now.

Edoardo Zarghetta, Managing Partner, IPO CLUB

New allocation · IPO CLUB II · Closes 14 August

Invest alongside the thesis: Blue Origin.

IPO CLUB has opened a single-company SPV into Blue Origin's ~$130B financing round, entered at the round price. $50,000 minimum, capped at 100 investors. Fees apply; full terms in the memo.

For twenty-five years, Blue Origin has been the company that did not need anyone's money. Jeff Bezos founded it in 2000 and funded it himself, reportedly on the order of a billion dollars a year in Amazon stock, and the rest of the market watched a generously financed space program build slowly and say little. That era looks like it is ending. In May 2026, the Financial Times reported the company was weighing its first-ever external fundraising round, and CEO Dave Limp told employees that hitting the company's launch-cadence targets would take more capital than a single backer could reasonably provide. He did not rule out a future IPO.

The timing is not an accident. In June 2026 SpaceX moved toward a public listing at a valuation north of $1.75 trillion, which would make it the largest IPO in history, and the gravitational pull of that event is being felt across every company with a rocket on its homepage. The obvious next question the market is already asking is: who is the next pre-IPO space name, and is Blue Origin it?

We think that framing skips the only question that actually matters. Blue Origin is not a story about whether space is a good place to invest. It is a single, specific bet, and it is worth saying the bet out loud: can capital plus time fix execution?

The honest ledger, both sides

Any serious look has to put both columns on the table, because the lazy versions of this story pick one and ignore the other.

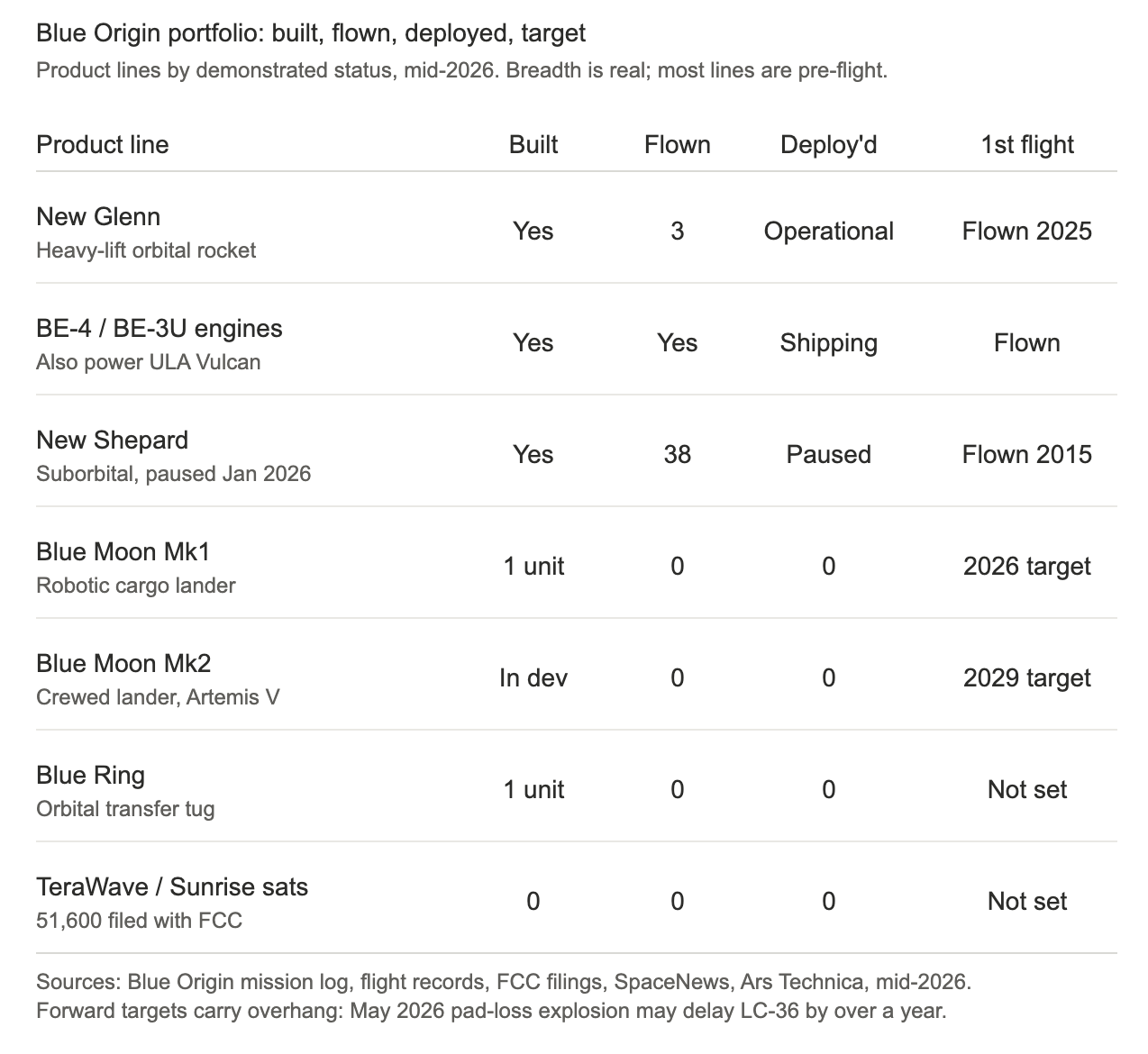

On the achievement side, the record is real. New Glenn, the company's heavy-lift rocket, reached orbit for the first time in January 2025. On its second flight in November 2025 it carried NASA's twin ESCAPADE spacecraft toward a Mars staging orbit and landed its reusable first stage on only the second attempt, something never before done with a booster that size. Blue Origin holds a $3.4 billion NASA contract for an Artemis V lunar lander. Its BE-4 engines power not only New Glenn but also United Launch Alliance's Vulcan, which makes Blue Origin a propulsion supplier to a competitor's rocket, a genuinely valuable franchise position. It holds a national-security launch contract in the most demanding tier of the Pentagon's program. And in March 2026 it filed with the FCC for Project Sunrise, a proposed constellation of up to 51,600 satellites aimed at orbital AI data centers, planting a flag in the same in-space-compute land grab that SpaceX and others are racing into.

On the setback side, the record is just as real and more recent. In April 2026, New Glenn's third flight suffered an upper-stage failure that left a commercial satellite short of its intended orbit. Then, on May 28, 2026, a New Glenn first stage exploded during a static-fire test at Launch Complex 36 in Florida, destroying the vehicle and severely damaging what is currently the company's only operational New Glenn pad. Industry reporting suggests repairs, or standing up an alternative pad, could take more than a year. The company's launch cadence is running at something like a tenth of its own stated targets.

Hold both columns in view at once and the real question sharpens. It is not "has the money produced anything," because it plainly has. It is narrower and harder: can the next tranche of capital convert specifically into cadence and reliability, the two things still conspicuously missing?

Blue Origin Porfolio Readiness

What the money was already supposed to do

Here is the uncomfortable part. The argument for a large external raise is that fresh capital lets Blue Origin scale, build, and finally hit the flight rate its plans call for. That is a perfectly reasonable thing for capital to do. It is also, almost exactly, what the previous decade and a half of Bezos's capital was supposed to do.

The company has consumed an enormous amount of money, by Bezos's own estimate on the order of $2 to $2.5 billion a year. It has produced real hardware and real contracts. What it has not produced, at least not in any form an outside investor can inspect, is published revenue, disclosed margins, or a stated backlog. After all of that spending and all of that time, the company remains, financially, a closed box.

So the honest version of the bull case is not "capital unlocks growth." It is "the next tranche of capital, unlike the last, finally converts into operational discipline and flight cadence." That may turn out to be true. But it is a claim about a change in execution, not a claim about a shortage of money. The two are easy to confuse and very different to underwrite, especially when the entry price being floated is a large one.

The halo is real, and that is the problem

When a category-defining company goes public at a historic valuation, it lifts everything around it. Capital floods in, comparable companies re-rate upward, and for a window of time the entire sector trades on the strength of the leader's story rather than on its own fundamentals.

That dynamic is good for the industry. It is more complicated for an investor trying to enter a specific name. A rising tide raises the price you pay to get in. The momentum that makes Blue Origin attractive to talk about is the same momentum that would set its entry valuation, and momentum-driven entry valuations are precisely the ones that make a strong eventual return harder to achieve, not easier. "The sector is growing" and "this is a good entry" are not the same sentence, even though they are often delivered as if they were.

Why the SpaceX analogy only goes so far

The instinct to map Blue Origin onto the SpaceX path is understandable, and it is also where most of the loose thinking happens. The two companies are not at the same place. SpaceX backs its valuation with billions in real revenue, a profitable consumer business in Starlink, and a launch cadence that dwarfs every competitor on Earth, well over a hundred orbital flights in a single year. Its public listing is the harvest of two decades of compounding operational wins.

Blue Origin is earlier on every one of those axes. It has reached orbit and landed a booster, real milestones, but its cadence is a fraction of its own targets and its most recent year includes two serious failures alongside the wins. Buying into "the next SpaceX" at a SpaceX-adjacent price means paying today for a track record the company has not yet built. The analogy sells the upside while quietly importing none of the evidence that justified it.

It is worth noting the counter-example trading in plain sight. Rocket Lab, a publicly listed space company, posts disclosed quarterly revenue, a real backlog, and published margins. You do not, it turns out, need private-market opacity to build a credible space business. That makes the absence of any comparable disclosure from Blue Origin a question to sit with, not wave away.

The founder backstop cuts both ways

There is a comforting version of the Blue Origin thesis that goes: Bezos will simply not allow a public failure, so the downside is protected. There is something to this. A founder with effectively unlimited resources and a personal stake is unlikely to let the company collapse.

But survival and a great investment are different outcomes. A company that never has to face a hard capital constraint is also a company that never has to develop the discipline that constraint forces. Patient, unlimited backing can keep a valuation propped up and an organisation comfortable at the same time. "It won't fail" is a floor on the company's existence. It is not, by itself, a path to the kind of return that would justify a high entry price.

The AI question, kept honest

The most imaginative version of the bull case points at Bezos's separate, heavily funded AI venture and imagines it folding into Blue Origin, the way other founders have combined their AI and hardware efforts. It is a fun idea. It is also speculation layered on speculation: it assumes the space round happens, assumes the combination happens, and assumes the result is good for a Blue Origin shareholder rather than dilutive to one.

More to the point, the visible evidence runs the other way. Bezos has described that AI venture as where the bulk of his attention now goes, and it raised its own enormous round at its own multibillion-dollar valuation. A fresh, separately capitalised AI company commanding the founder's focus reads more naturally as attention pointed away from Blue Origin than as a catalyst waiting to be merged into it. We would not put weight on this in either direction until something concrete supports it.

So what is the actual question to answer?

Strip away the halo, the analogy, and the speculation, and you are left with a small number of things that genuinely decide the case:

Does the new capital come with, or produce, a real change in execution? Cadence and reliability are the test, not the size of the raise, and the 2026 failures raised the bar for what counts as proof.

Is there a path to genuine transparency? An investor cannot underwrite a closed box forever. At some point revenue, margin, and backlog have to become visible, the way they already are at a public peer.

Does the entry price leave room for the outcome to matter? A great company bought at a halo-inflated price can still be a mediocre investment.

None of these is answered by the excitement around a SpaceX listing. They are answered by Blue Origin, over time, doing the things it has not yet done.

For more in-depth reports, become an IPO CLUB Member, or if you are an Advisor, continue to the Advisor Desk

Disclaimer

Private companies carry inherent risks and may not be suitable for all investors. The information provided in this article is for informational purposes only and should not be construed as investment advice. Always conduct thorough research and seek professional financial guidance before making investment decisions.

IPO CLUB Research

The full research lives inside the Data Room

Company deep dives, quarterly valuations, and live allocations across Defense, Energy, AI Infrastructure, Robotics, Critical Minerals, and Space. Membership is free.

Enter the Data Room → For accredited investors